The 3PL Consolidation Wave: What It Means When Your Competitor Gets Acquired

There is a question that more 3PL operators are sitting with in 2026 than at any point in recent memory.

What happens to my business if the company I compete against every week gets bought by a private equity firm or acquired by a national player?

It is not a hypothetical. The pace of merger and acquisition activity in the 3PL sector has accelerated sharply through the first half of 2026, with 48 deals completed year to date, a 20% jump from the same period last year. Private equity has returned to the sector with conviction. Strategic buyers are acquiring for technology capabilities, not just capacity. And the market is evolving in a way that has real consequences for every operator in the mid-market.

This post is a clear look at what is driving the consolidation wave, what it actually means for your business when a competitor gets acquired, and what the operators best positioned to grow through this period are doing differently.

The Numbers Behind the Wave

Those numbers tell a specific story. Private equity has $2.6 trillion in dry powder globally and is actively deploying it into logistics. The 3PL sub-vertical is the most acquired logistics category by deal count over the past three years. And the valuation gap between technology-enabled operators and commoditized ones has never been wider.

According to Capstone Partners, the M&A market is, in their words, bifurcated. Technology-enabled and specialized 3PLs are commanding strong buyer interest and premium multiples. Commoditized operators are finding limited access to capital and, in many cases, limited options outside of distressed sale scenarios.

Understanding which side of that divide your business sits on is one of the most important strategic questions a 3PL operator can answer right now.

What Is Actually Driving Buyers to the Table

The consolidation wave in 3PL is not random. Buyers are making calculated decisions about what they want, and the pattern is clear when you look at where the deals are landing.

Technology Capability Is the Primary Target

Strategic acquirers are buying technology, not just trucks and warehouse space. Echo Global Logistics acquired ITS Logistics in January 2026 to combine technology-enabled transportation management with ITS's specialized fulfillment and dedicated capacity capabilities. Descartes Systems has completed 36 acquisitions since 2016, consistently targeting software, AI, and fleet management niches that would take years to build organically. Nippon Express's CAD $1.8 billion acquisition of Metro Supply Chain Group, the largest in NX Group history, brought a tech-forward platform into their global network.

The thesis is consistent across buyers: it is faster and cheaper to acquire technology capability than to build it. And in a market where 74% of shippers say they would switch 3PL providers based on AI capabilities, acquiring technology-enabled operators is a direct path to winning and retaining that shipper base.

Scale and Network Density

Beyond technology, buyers are acquiring for geographic coverage and network density. The top nine 3PL players currently control roughly half of total market share, and that concentration is increasing. Larger operators are acquiring mid-size regional players to fill network gaps, adding warehouse footprints near major population centers, and consolidating management transportation capabilities across geographies.

For brands evaluating 3PL providers, this creates a preference for partners with national reach and demonstrated scale. That preference accelerates the dynamic where smaller operators without compelling differentiation find themselves squeezed on both ends: too small to compete with the nationals on scale, not differentiated enough to compete on value.

Geopolitical and Trade Volatility

Tariff volatility and trade disruption have accelerated demand for more sophisticated logistics services. Brands that were managing supply chains on autopilot are now actively seeking 3PL partners who can navigate complex, shifting conditions. Acquisitions of providers offering managed transportation, cross-border services, and freight visibility have spiked threefold year over year in 2026.

This is creating a specific acquisition premium for 3PLs with demonstrated capability in complex, compliance-heavy, or cross-border freight. If that describes your operation, the M&A environment is favorable. If it does not, the competitive pressure from acquired and better-resourced competitors is increasing.

What Happens to Your Business When a Competitor Gets Bought

This is where the conversation gets specific. When a 3PL you compete against regularly gets acquired by a PE-backed platform or a national player, several things typically happen, and most of them increase the pressure on operators who have not differentiated themselves.

They Get Resources You Do Not Have

Post-acquisition, a mid-size 3PL backed by private equity or integrated into a national platform gets access to capital, technology, and operational infrastructure that was not available to them as an independent operator. Their billing gets automated. Their carrier relationships get renegotiated at higher volume. Their proposals get more polished. Their client portal goes live.

The competitor you were quoting against six months ago at a similar capability level is now showing up to RFPs with a significantly better technology story. That shift can happen within a single quarter of a deal closing.

Your Shared Clients Start Getting Pitched

PE-backed acquirers are explicitly focused on revenue growth post-acquisition. That means the brands you share with an acquired competitor will receive outreach. The pitch will be straightforward: your current provider just became part of a larger, better-resourced platform with national scale, advanced technology, and capabilities your current provider does not offer.

Clients who are satisfied but not deeply committed, the ones who stay because switching feels like a hassle rather than because they genuinely value the relationship, are the most vulnerable to this outreach. If your value proposition is primarily price and convenience rather than specific capability and relationship depth, that pitch lands harder than you want it to.

The Valuation Benchmark Shifts

For operators thinking about their own eventual exit, watching technology-enabled competitors command 9 to 12 times EBITDA in acquisitions while commoditized operators trade at 5 to 8 times is a data point that matters. The gap between what a technology-enabled 3PL is worth and what a traditional operator is worth has widened significantly and is continuing to widen.

Every quarter that passes without investment in technology capability is a quarter where the gap between your potential exit valuation and a technology-enabled competitor's grows larger.

The Brands Watching From the Sidelines

There is another audience observing this consolidation wave that does not get enough attention: the brands themselves.

When a 3PL gets acquired, the brands using that provider face an immediate and reasonable question. What does this mean for my service? Will the account team change? Will pricing change? Will the operational focus shift as the new owner pursues integration and growth targets?

These questions create a window. Brands in transition are more open to evaluating alternatives than at any other point in the relationship. And what they are looking for in that evaluation has changed.

What brands want from a 3PL in a consolidation environment

- Stability. They want a partner they can count on not to be absorbed into a platform that changes everything about how the relationship works.

- Transparency. They want real-time access to their data, accurate billing, and clear reporting that does not require a phone call to understand.

- Flexibility. They want payment terms and service configurations that fit their business, not a standardized offering built for the acquiring company's platform.

- Technology. They want a partner whose operations are AI-enabled, whose billing is automated, and whose proposals are backed by data rather than estimates.

The operators who can answer all four of these clearly and specifically win the brands that move during consolidation disruption.

The Bifurcated Market Is a Real Opportunity If You Position for It

Here is the part of the consolidation story that does not get told enough: the bifurcation Capstone Partners describes is not just a threat to operators without differentiation. It is an opportunity for operators who have it.

When a major competitor in your market gets acquired and their clients start asking questions about stability and service continuity, those clients are available in a way they were not before the deal. The 3PL that can walk into that conversation with a clear technology story, a branded client portal, accurate automated billing, and flexible payment terms through embedded lending is not competing against the acquired company. It is competing against the uncertainty that acquisition creates.

That is a winnable conversation. And it is happening right now in markets across the country as the consolidation wave continues.

What the Operators Winning Through Consolidation Are Doing

The pattern among 3PLs that are actively growing through this period rather than being squeezed by it is consistent. They are not necessarily larger than their competitors. They are better differentiated.

The operators on the left side of that table are not immune to consolidation pressure. But they are competing on dimensions that acquired competitors cannot instantly replicate, because technology capability is not something a PE firm can inject overnight. It takes time to implement, integrate, and operationalize. The operators who have already done that work have a genuine window.

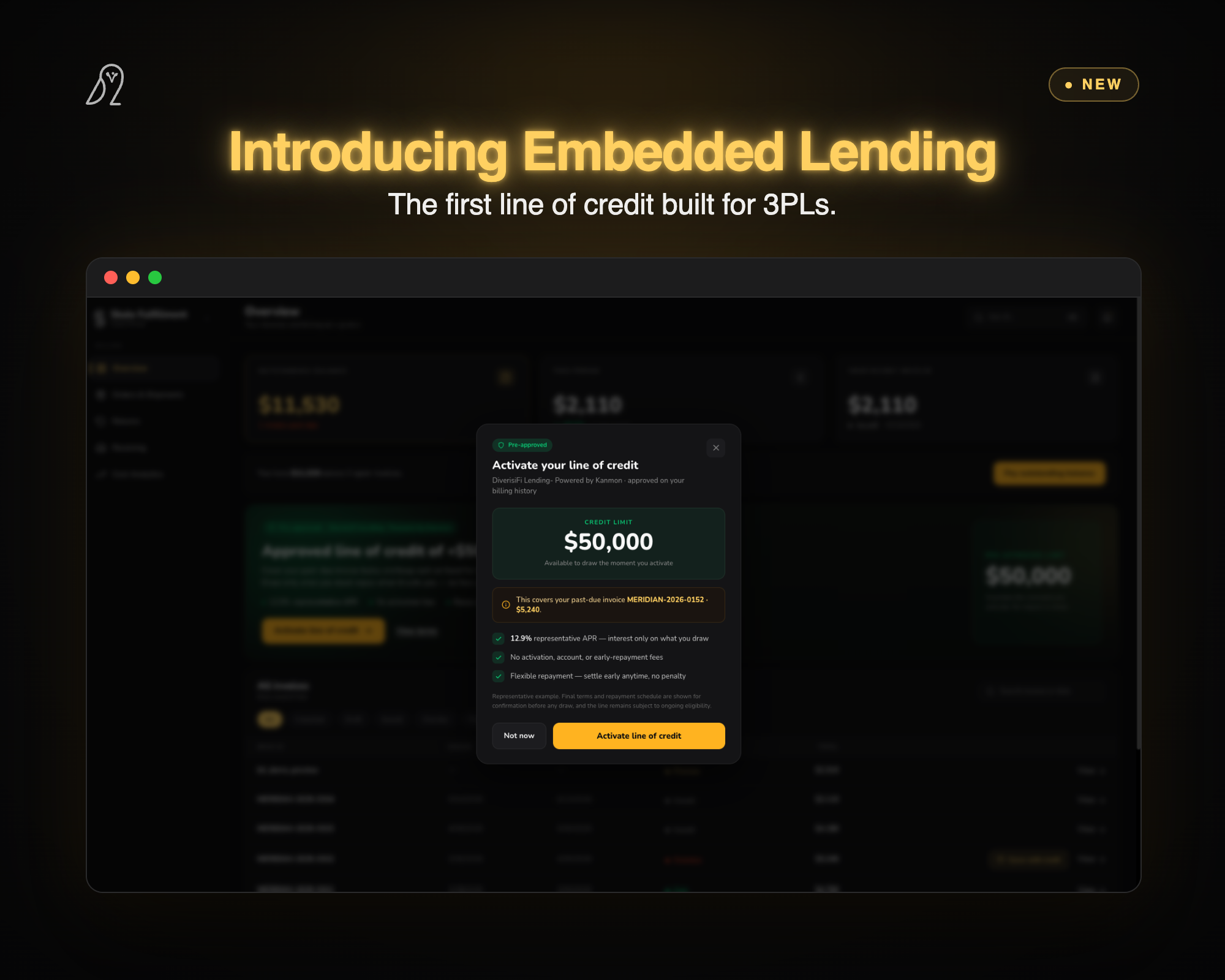

How DiversiFi Helps 3PLs Position for This Market

DiversiFi is built specifically to help mid-size 3PL operators compete as technology-enabled businesses in a market that is increasingly rewarding exactly that. The platform brings together AI Dynamic Billing, AI Carrier Routing, Bid Boost, the Client Portal, and Embedded Lending in one connected system, so the technology story you bring to a client or prospect conversation is real and demonstrable, not aspirational.

When a brand's current 3PL gets acquired and they start asking questions, you want to be the operator they call. When a prospect is evaluating three providers and one of them just became part of a national platform, you want to be the independent alternative with better technology and a more accountable relationship.

Both of those conversations are easier when your platform is already doing what the nationals are promising to do someday.

If you want to understand where your operation stands on the technology differentiation spectrum relative to the current market, we offer free cost modeling and a platform walkthrough that maps your current processes against what automated systems would deliver. Most operators find the gap is closeable faster than they expected, and the returns start compounding from the first billing cycle.

The consolidation wave is not slowing down. The operators who move now are the ones who will be taking clients from the disruption it creates, not losing them to it.

Frequently asked questions

What is 3PL software?

What is 3PL bidding software?

Continue learning

See AI for your 3PL In Action

Discover how our solutions can drive your success.