The State of 3PL Technology in 2026: What Operators Are Investing In and Why

A lot has happened in logistics over the past 18 months. Carrier surcharges have climbed to levels most operators had not planned for. Amazon opened its logistics network to any business that wants to use it. Private equity flooded back into the 3PL sector, and M&A activity accelerated through the first half of 2026 at a pace not seen since 2021. Tariff volatility reshaped sourcing decisions almost overnight.

Through all of it, one thing became increasingly clear: the 3PLs that navigated this period better than their competitors were almost universally the ones that had invested in technology ahead of the disruption, not in response to it.

This post is a look at where the industry stands right now, what operators are actually investing in, what the data says about where things are heading, and what it all means if you are running a 3PL in 2026 and thinking about where to put your next dollar.

The Numbers First

Before getting into what is driving investment decisions, here is a snapshot of where the 3PL technology landscape sits right now.

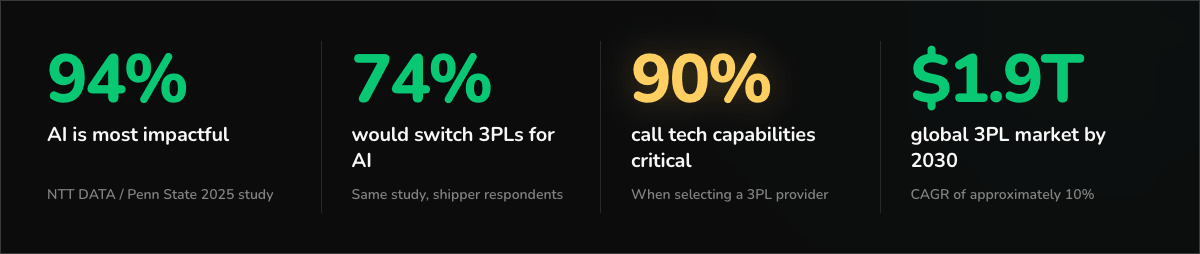

That 94% number is the one that stands out most. When the NTT DATA and Penn State University 2025 Third Party Logistics Study asked respondents which technologies were most impactful to logistics, AI came back at 94%. Driverless vehicles, which dominated the conversation five years ago, came in second at 46%. The gap between AI and everything else is large and growing.

The 74% switching statistic is the one that should get the attention of every 3PL operator who has not yet made AI a visible part of their service offering. Three out of four shippers are willing to move their business based on AI capabilities. Not price. Not geography. AI.

And the 90% figure is where the accountability sits. Almost every shipper says technology is critical when they choose a 3PL. Only 57% say they are satisfied with their current provider's technology capabilities. That gap is not a statistic. It is an open door.

What the Money Is Actually Going Into

If you look at where 3PLs of all sizes are directing technology investment in 2026, five categories dominate the conversation. Some are warehouse-floor investments that most mid-size operators are still working toward. Others are operational and financial tools that are available and generating returns today.

AI and Billing Automation

For mid-size 3PLs, this is where the most immediate and measurable ROI sits. AI billing automation, which matches carrier invoices against shipment records, applies current rate cards automatically, and captures surcharges in real time, is not a future capability. It is available now, it pays back within a single quarter for most operators, and it eliminates one of the most persistent sources of margin leakage in the business.

The current carrier surcharge environment makes this more urgent than it has ever been. Fuel surcharges across UPS, FedEx, USPS, and Amazon have risen sharply through 2025 and 2026. A 3PL billing clients at last quarter's surcharge rate while paying this quarter's higher carrier costs absorbs the difference on every affected shipment. At 5,000 shipments per month, that absorption is not a rounding error. It is a significant annual loss.

Billing automation closes that gap structurally. And when billing data is connected to bidding and carrier routing, the value compounds. The same data that makes invoices accurate also makes proposals more precise and carrier negotiations more credible.

AI Carrier Routing and Optimization

Static routing guides are a liability in the current environment. When surcharge rates are moving quarterly and carrier performance varies by lane, a routing guide built last year is already out of date. AI carrier routing evaluates the real cost and performance profile of each carrier for each shipment in real time, accounting for current surcharges, delivery history, and service level requirements before making a decision.

For 3PLs managing volume across multiple carriers, the margin improvement from dynamic routing versus a static guide can be significant, particularly on lanes with high surcharge exposure or variable performance. It also changes the conversation with carriers at contract time. When you can walk into a negotiation with specific data on your lane level volume, service performance, and cost history, you are negotiating from a different position than someone coming in with a general sense of what they ship.

Warehouse Automation

This is the category getting the most attention at the enterprise level, and understandably so. The warehouse robotics market reached $9.33 billion in 2025 and is projected to more than double to $21 billion by 2030. Major 3PLs are now directing 40% to 50% of their capital expenditure into technology and automation, with autonomous mobile robots, automated storage and retrieval systems, and robotic picking all moving from pilot programs into standard operations.

For mid-size operators, the Robots as a Service model has changed the access question. Rather than a multi-million dollar capital outlay, RaaS contracts convert automation into a usage-based operating expense. That is a meaningful shift in who can deploy automation, and it is accelerating adoption across the mid-market.

That said, warehouse automation has a longer payback timeline than billing or routing software for most operators, and the implementation complexity is real. It is an investment to plan toward rather than one that generates returns in the first quarter.

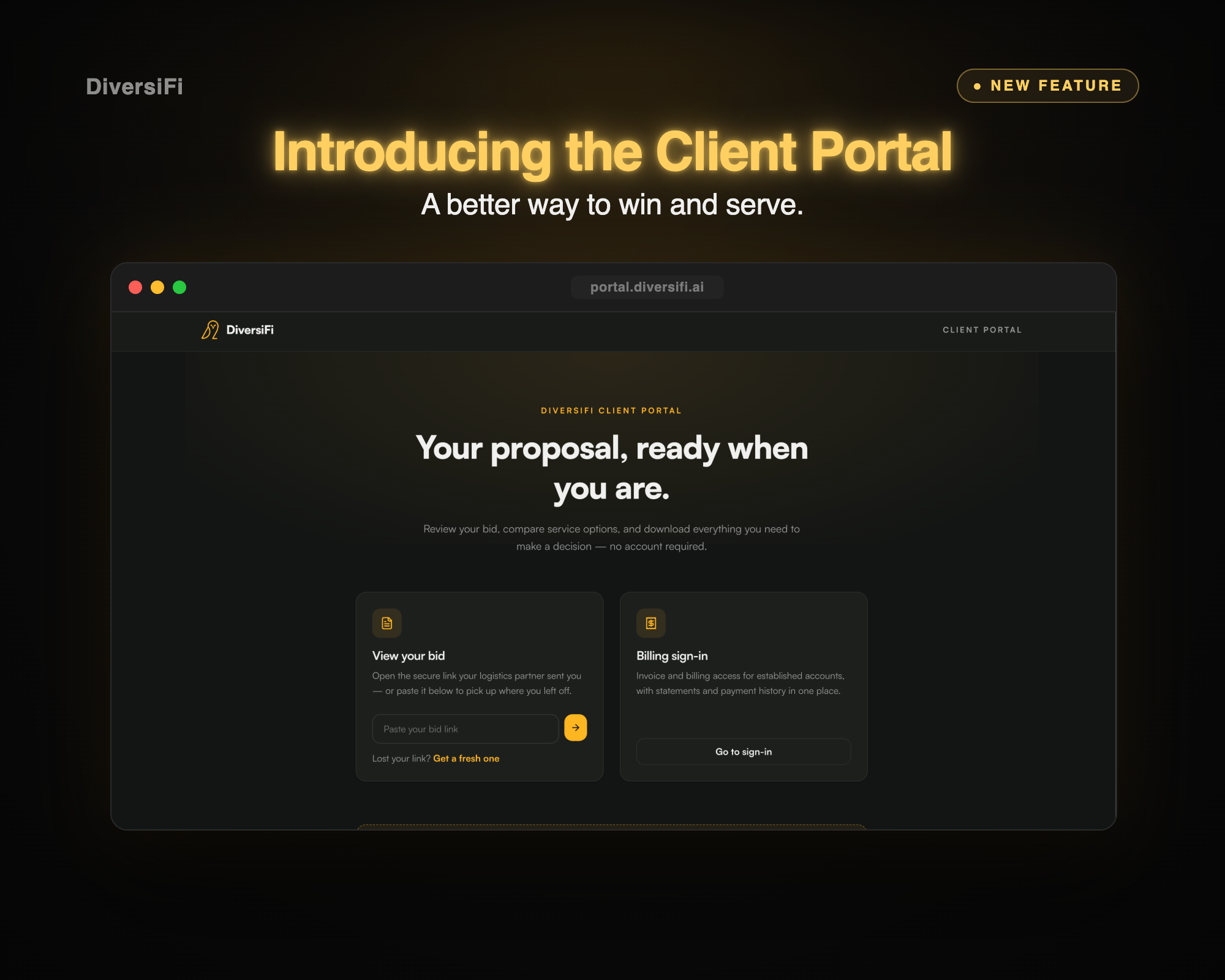

Supply Chain Visibility Platforms

The NTT DATA study found that 61% of shippers believe change management is needed specifically to improve supply chain visibility. Clients want to know where their freight is, when it will arrive, and what it is costing them, in real time, without having to call someone to find out.

For 3PLs, investing in visibility tools is both a client retention play and a competitive differentiator in new business conversations. When you can offer a client real time access to their operational data and billing through a branded portal, the relationship dynamic changes. They are not dependent on you to answer basic questions. They have the data when they need it, and the experience of accessing it reflects well on your operation.

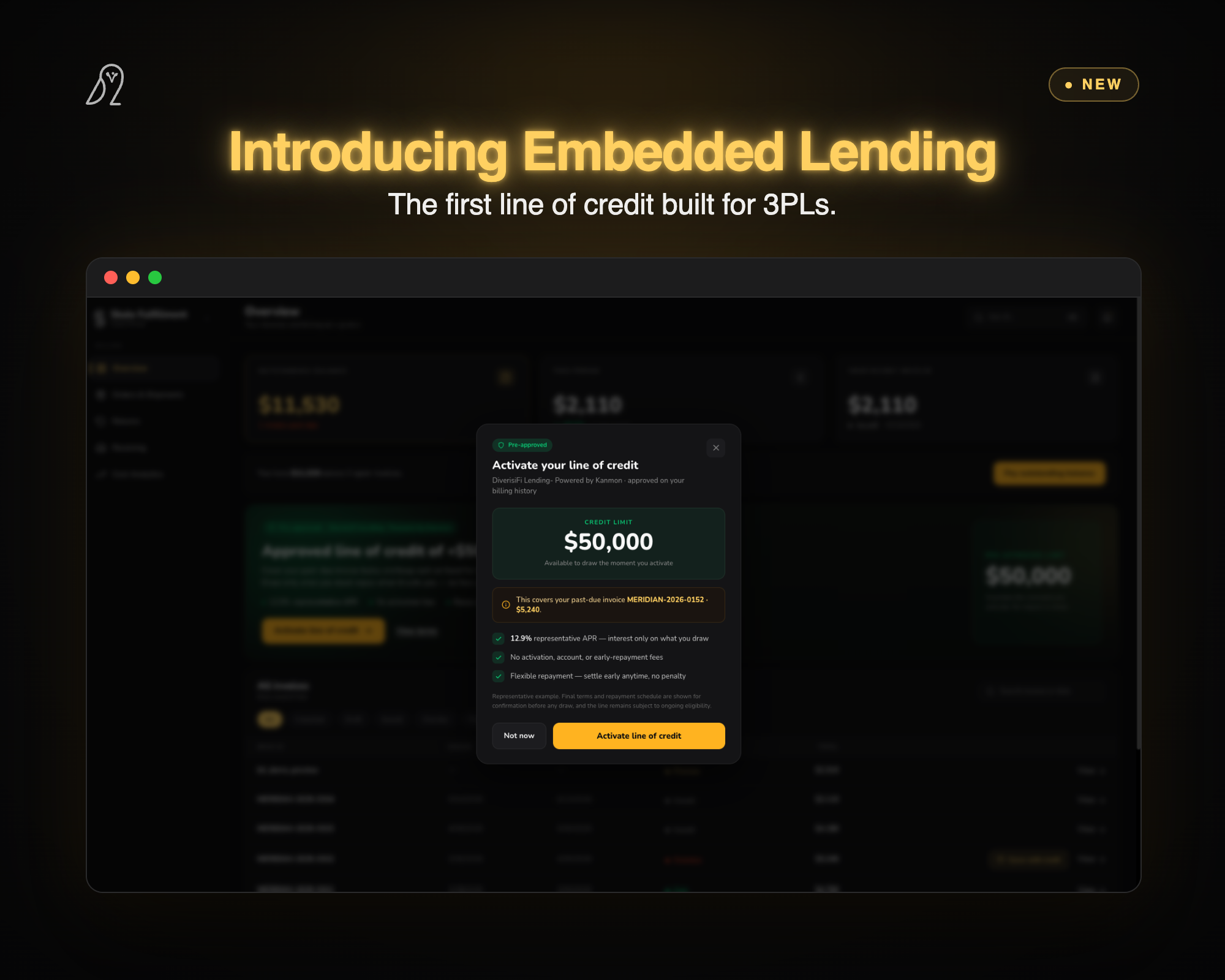

Embedded Financial Tools

This is the newest category and the one that is creating the most competitive separation between operators who have moved on it and those who have not. The structural cash flow problem in 3PL operations, where carriers get paid in 7 days and clients pay in 30 to 90, has historically been managed through deposits, tight payment terms, or simply absorbing the gap with working capital.

Embedded lending tools change that equation. When an integrated line of credit bridges the carrier payment gap automatically, 3PLs stop floating cash on every shipment cycle. And when they can offer clients flexible payment terms without absorbing the financial risk themselves, they compete on a commercial dimension that most of their competitors cannot match.

This is still an early category in the 3PL technology stack, but the operators who move on it first are gaining a sales and retention advantage that is not easy for competitors to close quickly.

The Market Pressures Making This Urgent

Technology investment in 3PL operations has been a priority for years. What has changed in 2026 is the urgency. Several converging forces are making the gap between tech-enabled and non-tech-enabled operators more consequential than it has ever been.

M&A Activity and the Consolidation Effect

Private equity has returned to the 3PL sector with focus. Through the first half of 2026, PE transaction activity has accelerated, with 23 deals completed year to date, up from prior periods, driven by late 2025 interest rate cuts and a clear buyer thesis: technology-enabled 3PLs command better multiples and generate stronger returns than traditional operators.

Thoma Bravo's acquisition of WWEX Group for an estimated $5 billion enterprise value in March 2026 is the headline number, but the pattern runs deeper. Buyers are specifically targeting 3PLs with automation capabilities, AI-enabled operations, and platform-driven efficiency. The top nine 3PLs now control roughly half of total market share, and that concentration is increasing.

For mid-size operators, this creates a dual pressure. The large players are deploying technology at scale with PE-backed resources. And the market is rewarding tech-enabled operators both in terms of client acquisition and exit valuation. The operators without a technology story are getting squeezed from both ends.

What this means in practice

A brand evaluating three 3PLs right now is seeing a widening capability gap between the operators who have invested in technology and those who have not. The tech-enabled operator can offer automated billing with full transparency, a branded client portal with real time analytics, flexible payment terms through embedded lending, and AI-powered routing that documents cost optimization on every lane.

The operator running on spreadsheets and a static routing guide is competing on price and relationship. In a market where 74% of shippers say they would switch providers based on AI capabilities, that is an increasingly difficult position to defend.

Amazon's Entry Into Open Logistics

Amazon Supply Chain Services launched in May 2026, opening Amazon's full logistics network to any business. Freight, warehousing, fulfillment, and parcel delivery, available to any brand, at Amazon's scale and pricing leverage.

For 3PLs serving e-commerce brands, this is a direct competitive pressure. For operators in specialized verticals or with strong technology differentiation, it is less immediately threatening but still reshapes the conversation brands have with their logistics partners.

The 3PLs best positioned to compete against Amazon's entry are those who can offer something Amazon's standardized network cannot: customized service levels, transparent and accurate billing, flexible financial terms, and a client experience that feels like a genuine partnership rather than a platform relationship.

Carrier Surcharges and Cost Volatility

The surcharge environment has been one of the most operationally consequential developments of the past 18 months. UPS ground is at 22.25%, FedEx at 22.50%, USPS added 8% in April 2026, and Amazon added a 3.5% logistics surcharge. Geopolitical instability has pushed some international surcharges above 40%.

For 3PLs billing manually, this environment is a persistent margin threat. For those with automated billing and dynamic routing, it is an advantage, because their systems capture every surcharge change accurately and route volume to the most cost-effective carrier on every lane.

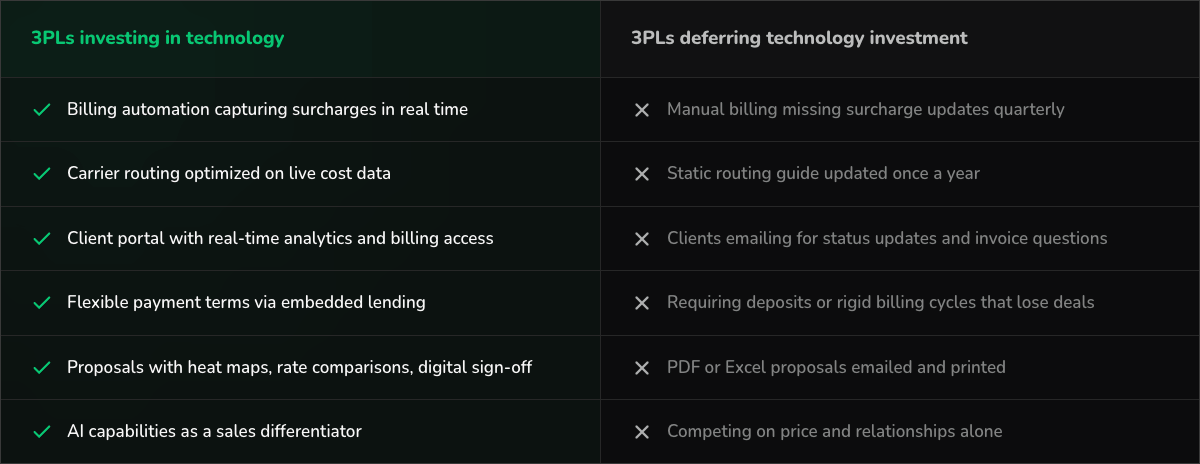

What the Gap Between Leaders and Laggards Looks Like

Here is the practical picture of how technology investment is separating operators in the current market.

The gap in the table above is not theoretical. It is playing out in sales conversations and renewal discussions across the industry right now. The 3PLs on the right side of that table are not necessarily doing anything wrong. Many of them are well-run operations with strong client relationships and solid operational fundamentals. But they are competing against an increasingly technology-differentiated market with tools that were built for a different era.

Where to Start If You Are Behind

If you are reading this and recognizing that your technology story needs work, the good news is that the path forward is clearer than it has ever been. You do not have to solve everything at once, and you do not have to start with the most complex or expensive investments.

The highest ROI starting point for most mid-size 3PLs is billing automation. It generates measurable returns within the first quarter, it directly addresses the margin leakage that is already happening in your operation, and it builds the data foundation that makes every subsequent technology investment more valuable. Accurate billing data feeds better bidding decisions. Better bidding data improves carrier negotiations. Better carrier data informs routing optimization.

From there, the progression is natural. A connected billing and routing platform gives you the data to compete more aggressively in sales conversations. A client portal gives your clients a professional, transparent experience that reduces churn. Embedded lending gives your sales team a commercial differentiator that closes deals other operators cannot.

None of this requires building from scratch or replacing your entire technology stack. The most effective approach is targeted deployment in areas with the clearest return, connected to the systems you already use. The right partner makes the integration timeline weeks rather than quarters.

The Recap

The 3PL technology landscape in 2026 is not particularly complicated to read. The operators who invested in technology in 2024 and 2025 are winning more business, retaining more clients, and managing margin more effectively than those who did not. The market data is clear on that. The shipper data is even clearer.

The question for any 3PL operator right now is not whether technology investment matters. It is how quickly you move, and where you start.

The gap between technology leaders and laggards is widening every quarter. The cost of closing it goes up the longer you wait. And the returns, when you do invest in the right areas, show up faster than most operators expect.

If you want to understand where your operation stands relative to the technology benchmarks in this post, DiversiFi offers free cost modeling that maps your current billing, routing, and cash flow processes against what automated systems would deliver. It is a useful starting point before making any investment decisions.

The state of 3PL technology in 2026 is clear. The only question left is where your operation fits into it.

Additional Sourcing

Frequently asked questions

What is Amazon Supply Chain Services and how does it compete with 3PLs?

What is AI carrier routing and how does it work for 3PLs?

How is AI being used in 3PL operations?

Continue learning

See AI for your 3PL In Action

Discover how our solutions can drive your success.